Executive Talk

As Thailand works to expand financial inclusion and uplift its vast network of small business owners, Thai Credit Retail Bank Plc (CREDIT) has emerged as a fast-growing force driving change at the heart of the informal economy. In this interview, Chief Executive Officer Mr. Roy Agustinus Gunara explains how the Bank has carved out a distinctive position in the national banking landscape — prioritising micro-SME lending, relationship-based services and a forward-looking digital transformation designed to unlock opportunities for millions of entrepreneurs traditionally excluded from mainstream finance.

What is the history of CREDIT?

Thai Credit began as a credit foncier business in the 1970s. When the Bank of Thailand opened new banking licences, the shareholders applied on the strength of their capital base, received a licence in 2006 and commenced operations in 2007. In 2012, the current management team introduced a new plan centred on micro-SME lending, restructured the Bank and began a full transformation. In 2015, CREDIT launched its nano loan business, building core capabilities internally.

“We chose micro-SME because it was a clear gap in the market,” Mr Gunara explains.

“Thailand has a large underground and underserved economy with limited access to capital and few institutions willing to serve informal businesses without tax records or proper bookkeeping.”

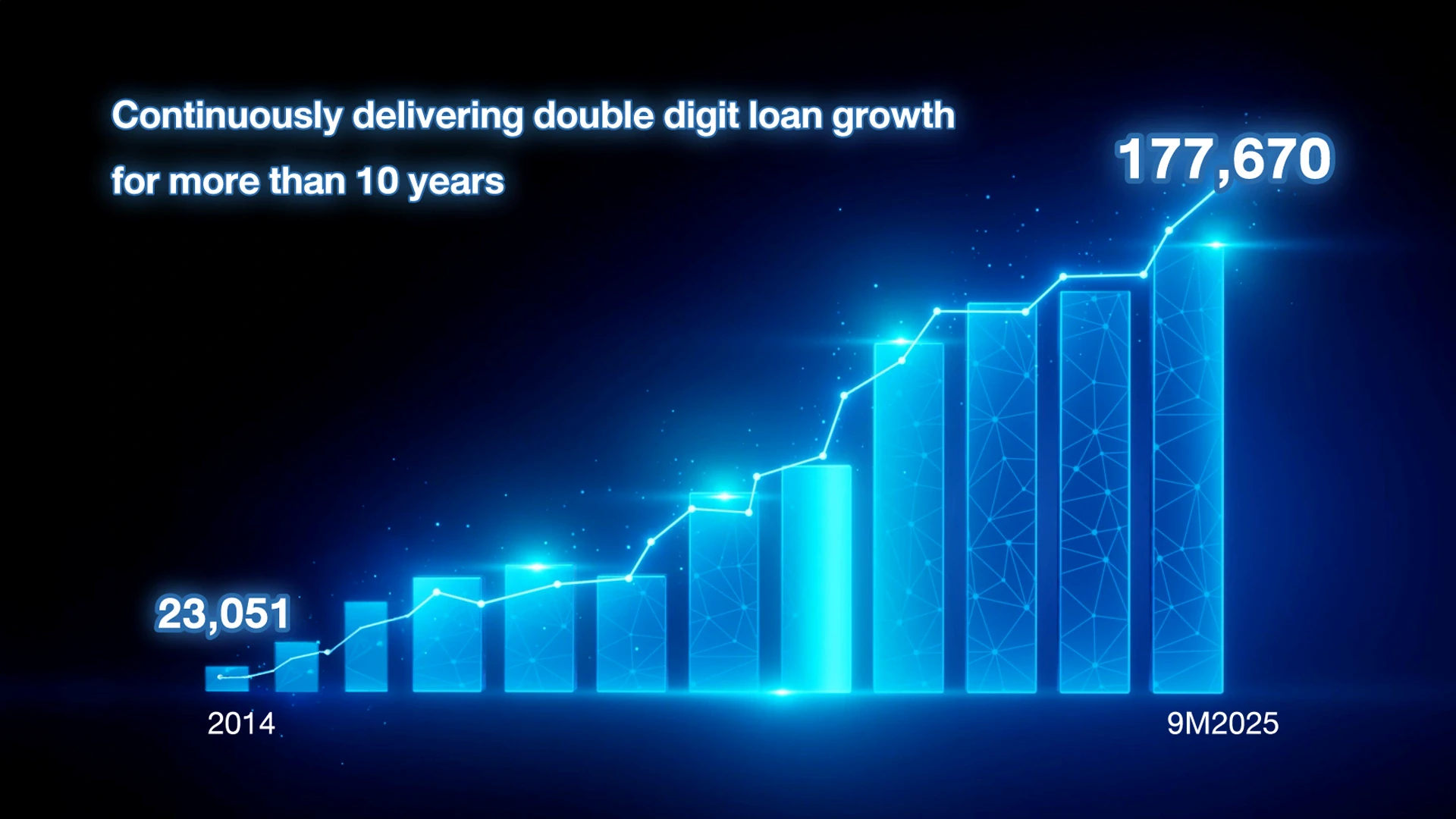

Historically, many operators relied on personal loans, car-for-cash products and other high-cost borrowing options. The Bank initially managed about THB 20 billion in assets in 2012 across SME, home loan and auto-loan portfolios, but found those segments too competitive and pivoted toward micro-SME. The loan book has since grown to around THB 180 billion — delivering annual growth of approximately 20–30% — and CREDIT has been profitable since the second year of this model.

SMEs and micro-SMEs are commonly used terms in the banking industry. How does CREDIT define them?

“Our core customers are business owners — small shops, small merchants and family-run operations,” he says. “Many have little or no collateral and may not qualify for retail or credit card loans.”

The Bank serves micro and nano borrowers with loan limits of roughly THB 100,000–200,000, generally with fewer than five employees and limited formal records. Approximately THB 20 billion of the nano and micro portfolio comes from around 250,000 customers, while about THB 150 billion is attributed to customers with larger exposures and other business segments.

What are the main differentiators of CREDIT in Thailand’s highly competitive banking sector?

“Our key differentiator is our deep focus on micro-SME customers,” Mr Gunara explains. “We strategically target small, often informal business owners who are largely invisible to bigger banks and have limited access to standard SME products.”

Rather than treating these clients as personal loan borrowers, CREDIT recognises them as business owners — a mindset that demands a tailored underwriting approach, hands-on relationship management and a distinctly specialised operating model.

Over more than a decade, the Bank has developed a dedicated micro-SME platform comprising low-cost lending branches, intensive staff training in credit and relationship skills, and a culture anchored in the belief that “Everyone Matters.”

CREDIT also positions itself in comparison with commercial banks rather than government lenders, with a focus on business customers rather than agricultural lending, using its lean structure and specialist expertise as a sustainable advantage.

What is the current business model focus — retail, SME, micro-SME or digital banking? How will this evolve?

“Our core focus remains micro banking and small businesses, defined as those operating below the conventional medium enterprise scale,” he says. Management believes this market is significantly larger than commonly recognised due to the size of Thailand’s informal economy, offering extensive room for growth.

While the broader banking market is framed around SME, consumer and corporate segments — with the top five banks dominating SME lending — CREDIT aims to lead the micro-SME segment and expand through digital banking.

“The Thai banking sector has not yet experienced true digital disruption, as many so-called digital platforms still run on legacy cores,” he notes. Over the past two years, CREDIT has launched a mobile banking platform and is accelerating further investment in technology, acknowledging that genuine digital transformation will take time but will be essential for the next phase of growth.

How has the “Everyone Matters” philosophy impacted strategy and operations?

Introduced a decade ago, the “Everyone Matters” philosophy has shaped both CREDIT’s strategy and culture. It reinforces a business model designed to genuinely serve small, often overlooked customers — treating them as business owners rather than personal-loan borrowers. The emphasis is on relationship-based lending and a culture of genuinely caring for customers, reflecting Thai values such as kreng jai.

This philosophy is also expressed through the Bank’s long-running financial literacy programme. A dedicated team of around 25 specialists, supported each year by 500–700 employee volunteers, delivers training to approximately 60,000 participants nationwide via partnerships with OTOP, the Ministry of Interior, schools and universities. With more than 20 engaging and practical training modules, the programme focuses on essential financial skills such as saving, record-keeping and avoiding over-leverage — and has received strong positive feedback from micro and nano business owners.

“We do not view this as CSR or business acquisition,” Mr Gunara stresses. “It is about strengthening our communities and helping small businesses thrive.” No loans are sold or products promoted at these sessions, preserving the programme’s integrity. Instead of large marketing budgets, CREDIT builds brand trust organically — through service, education and community impact.

What are the biggest opportunities for CREDIT in the next 3–5 years?

CREDIT sees three major opportunities ahead: deepening penetration into the micro-SME sector, improving productivity through digital transformation and expanding into new customer segments using its developing digital platform.

The informal and micro-SME economy in Thailand remains significantly underserved, and the Bank estimates its current market share at around 2% — indicating substantial room for continued growth. CREDIT has already invested heavily in its new digital platform with the goal of becoming a full digital bank within a few years. New products are being prepared to reach underserved groups through fully digital channels.

Around half of CREDIT’s customers have already shifted from cash to digital transactions through one of its e-wallet channels. Increasing this adoption will further enhance productivity, reduce friction and elevate the customer experience.

Can you summarise CREDIT’s key financial achievements over the last 2–3 years?

“Our micro-SME model has continued to deliver resilient growth and strong profitability,” says Mr Gunara. “Although we remain a relatively small bank, we believe we have been one of the fastest-growing in Thailand for more than a decade.”

The Bank’s loan book has expanded from around THB 20 billion at the beginning of its strategic pivot in 2012 to approximately THB 180 billion today — supported by consistent and disciplined profit growth throughout this period. The portfolio includes roughly THB 20 billion in nano and micro loans to around 250,000 customers and around THB 100 billion to a smaller group of customers with larger loan sizes.

On the funding side, CREDIT operates 33 deposit branches managing around THB 130 billion in deposits, with strong productivity per branch. Through prudent portfolio management and cost efficiency, the Bank has consistently delivered a return on equity between 15–20% — placing it among the highest performers in the Thai banking sector.

How does CREDIT manage credit risk, especially given rapid loan growth and economic cycles?

“As our model is high risk–high return, we manage risk very tightly,” Mr Gunara notes. CREDIT’s approach relies on relationship-based lending, a culture of genuinely caring for customers, and extensive training in underwriting, prudent collections and customer engagement.

Detailed local knowledge is a core advantage. The Bank has mapped nearly all traditional “Talat Thai” markets nationwide with more than 200 shops, and now serves around 90% of these markets through its lending branches. Even during a period when many banks were closing physical locations, CREDIT continued to expand using a low-cost branch format — with only a small number of sites yet to turn profitable.

This disciplined approach, combined with close monitoring and a focus on productive lending, has enabled CREDIT to maintain a relatively low NPL ratio compared with peers in similar loan-size segments, even in softer economic conditions.

Where do you expect to see CREDIT by 2030?

“Growth remains our most important strategy,” he says. CREDIT’s long-term ambition is to be among the top 10 banks in Thailand within five years and, by 2035, to be recognised as a leading institution — particularly for its role in serving micro-SMEs and the productive poor.

To achieve this, the Bank will continue expanding its core micro-SME and nano business, while diversifying into new areas on the strength of its evolving digital capabilities. The organization currently employs around 5,000 people — the majority being relationship managers and front-line staff who directly serve customers — supported by lean credit and back-office structures that allow efficient execution and rapid decision-making.